In general, the FY 2020 reporting season was much anticipated, particularly in light of the wholesale abandonment of company guidance at the heart of the COVID-19 sell-down, and a consensus view that was running relatively blind as many company balance sheets rapidly felt the challenges of COVID-19 changes in demand and supply.

Q: Ratio of earnings and dividend upgrades, downgrades, stable?

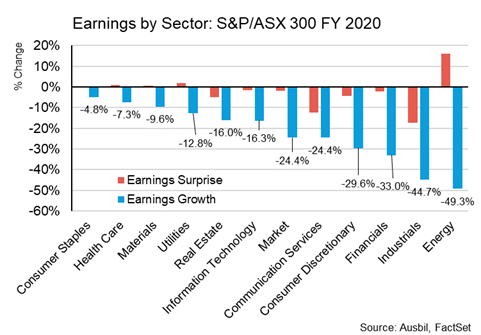

On earnings and dividends this reporting season, while many brokers report ratios of beats and misses, as our focus is earnings and earnings growth, we have looked at reporting season from the perspective of earnings impact. The following chart may be of assistance, showing Earnings by Sector for the financial year ending 30 June, and reported in August.

By the end of the August FY reporting season, the S&P/ASX 300 had delivered an average earnings surprise of -1.8%, and earnings contraction for the year of –24.4%. No sector delivered positive earnings growth, with just Utilities, Health Care, Materials and Energy delivering a positive earnings surprise (Energy related to the recovery in oil prices). Across reporting season, though consensus was relatively unreliable given the circumstances, the outlook for FY21 earnings growth shifted down from -0.7% to -1.1%, with FY22 compensating for a slight push-out for earnings from +14.4% before reporting season to +14.9% after. The rest of the sectors reflect, to differing magnitudes, the negative earnings impact of border closures and lockdowns, as illustrated in the chart.

On dividends, this reporting season, mining companies generated more dividend by value than did banks. The strong demand for iron ore is a particular standout this reporting season. To give you an idea of the magnitude, the top-four mining companies (BHP, FMG, NCM, RIO) paid a total dividend of A$20.4bn compared to the top-four banks (ANC, CBA, NAB, WBC) whose total dividend payments amounted to A$9.7bn, or less than half the miners. It is doubtful that such an occurrence will persist indefinitely, and as the economy recovers, which at this stage is expected to occur into 2021, we would expect to see bank earnings grow and dividends recover.

Despite Westpac deferring, then cancelling their dividend, CBA was able to declare at the top end of expectations, and ANZ have paid out their interim dividend that was previously deferred. NAB had already paid their dividend. We also saw strong performances from many retailers benefitting from the fiscal stimulus and a change in spending patterns away from services.

Q: Capital management initiatives of note?

On capital management, there were a few special dividends announced by companies with excess cash, for example, Wesfarmers following the sale of Coles, and Northern Star Resources, on the back of a very strong performance in the gold price. AMP, despite recent issues, also declared a special dividend following the sale of their life company.

On capital raisings, there were a swathe of small and large raising in the lead-up to reporting season to strengthen balance sheets.

Q: View on major bank and major miner results?

View on major miners. Ausbil’s long Australian equity portfolios have been overweight Materials, and major miners, for some time, particularly in leading Iron Ore, Base Metals and Rare Earths miners, on the continuing demand for resources from current global building and infrastructure programs, and on the view of a recovering economy heading into 2021. More recently, Ausbil has also been overweight select quality gold exposures in various portfolios such as Newcrest, Northern Star Resources and Saracen Mineral Holdings, adding some risk mitigation and hedging benefits in the current pandemic environment.

View on banks. If you are optimistic about Australian and New Zealand economic recovery, and we are, you have to be comfortable with the banks. The banks are most leveraged to an improving environment. We are seeing that already. Again, the dire expectations of three months ago, even two months ago, have improved markedly. Banks were provisioning for an economy with far higher unemployment levels than we have experienced, a deeper negative growth experience than has occurred, and a more elongated recovery than we are seeing at this juncture. Ausbil is currently overweight in ANZ, CBA and NAB, with WBC at a slight underweight, having added to positions when most were trading below book value in the recent sell-down. While this reporting season saw one cancelled dividend, and reduced dividends from others, our view on the banks relates to their key place in the recovery, which we expect to start in the second half of 2020, and strengthen into 2021. Economic recovery is expected to see bank earnings upgrades and, potentially, improved dividends.

Q: COVID impact on sectors and companies to note?

In understanding the market, it has become apparent that COVID-19 has accelerated a number of key demographic trends, and brought about a step-change in how people behave, much of which is unlikely to reverse.

The rise in the work-from-home phenomenon, triggered by lockdown measures, has proved-up a new working model, largely by necessity, but also because technology is now capable of supporting such changes. This has seen voluminous shifts to e-commerce for sales and service, the rapid localisation of supply changes, and a new kind of globalisation that can operate even without access to, and the cost of, interstate or intercontinental travel.

Market sectors, and their constituent companies, are showing these trends. Connectedness, data storage, cyber-security and compliance are now even more important as commerce increasingly shifts into cyberspace, driving performance in Information Technology and Communication Services. People are changing how they travel to work which is seeing greater usage of toll roads in the Transportation sub-sector of Industrials, and while they are home they have been spending on home improvement and renovation, education and localised and outdoor activities, all in the Consumer Discretionary sector. Traditional retailers are now more dependent on their e-commerce channels, rather than bricks-and-mortar stores, in both the Consumer Discretionary and Staples sectors, and medical treatment and advice is increasingly delivered through non-contact channels in the Health Care sector. Spending patterns are supporting a whole new, non-bank buy-now-pay-later sector, some of which are categorised as Information Technology, some Financials, all more connected to the consumer than ever through big data. There is a consequent boom in the warehouses and logistics infrastructures which support this explosion in online activity, and new real estate giants are in the making in the Real Estate / REIT sector.

The FY 2020 reporting season has seen the impact of these recent shifts, and accelerations in trends, in the performance of companies in our portfolio. It has also seen traditional sectors like Materials riding a wave of global demand, spearheaded by China’s ongoing growth, and in select energy exposures supported by the fundamental productive economic demand for energy. Ausbil has positioned its portfolios for this diverse pool of multi-sector opportunities, and with sharp focus on the strength of balance sheets, FY 2020 reporting season has been very positive for potential future out-performance.

Q: High level perspective on management outlook statements?

This reporting season, management has been very cautious about outlook statements, and understandably so. The onus is on proficient and informed investors to fundamentally value companies with a wide dispersion of potential future scenarios, and independently determine whether earnings upgrades are on the horizon, or not. We think there is even more opportunity here, however, we mitigate the dearth of guidance from companies through only investing in strong balance sheets and companies with ready access to liquidity for operation, and expansion.

Q: Other themes permeating from reporting season to note

Really, this reporting season served to underscore that some companies are resilient and thriving, some that have been hit hard by the pandemic are resilient and capable of waiting for things to change, and some are simply not strong enough to thrive. Balance sheet strength is the key, and the lack of material negative surprises this reporting season allows us to look forward at earnings potential as the economy recovers. With COVID-19, many industries and companies are reworking their operating models to be able to function under pandemic conditions. In the event of a vaccine discovery, economic recovery is expected to pull forward radically.

In the meantime, we remain of the view (subject to no further material deterioration in COVID-19 infection rates) that the pronounced decline in economic activity, as experienced in the first half of 2020, will be followed by a gradual recovery later in 2020, and building strength into 2021. We believe this recovery will be U-shaped as the world economy slowly returns to productivity, with or without a vaccine.

Source: Ausbil Investment Management Limited