Bill Shorten’s proposed changes to the dividend imputation system are a naked tax grab. They are not about making the system more equitable, and they are not closing a “tax loophole”.

The changes, which would see an end to the Australian Taxation Office paying cash refunds to taxpayers who have excess imputation credits, is set to raise $59bn over 10 years. To start from 1 July 2019, it will raise more than $5bn in its first year.

Self-funded retires and pensioners will be particularly hard hit, as will non-working spouses and part time workers who have share investments. In fact, anyone whose marginal tax rate is less than 30%, which includes all superannuation funds and persons with incomes under $37,000, could be impacted. At least 1.12m taxpayers will be worse off – and potentially a lot more if some public offer super schemes are also caught.

And because Bill and his team have a realistic chance at winning the next election, companies will act by bringing forward the payment of special dividends and off-market buybacks.

More on this later. First, let me explain why Shorten is not “closing a tax loophole” and why this is a naked tax grab.

ELIMINATE DOUBLE TAXATION

Dividend imputation exists to eliminate the double taxation of company profits. If a company makes a profit, it pays tax on that profit at 30%. If the company then pays a dividend out of its after-tax profit, that dividend is taxed in the hands of the shareholders at their marginal tax rate, which could be as high as 47%. The original profit has been taxed twice – once in the hands of the company, and once in the hands of the shareholders.

Paul Keating recognized that company profits were, through double taxation, effectively being taxed at punitive rates and introduced the system of dividend imputation in 1987. The system effectively rebates through imputation credits (also called franking credits) the tax that the company has already paid, so the profit is only taxed in the hands of the shareholder.

Critically, the system only recognizes company tax that has been paid to the Australian Taxation Office, so if companies aren’t paying tax in Australia, they can’t frank their dividends. This is why companies such as CSL, which earns more than 90% of its revenue outside Australia and pays tax to foreign governments, can’t frank its dividends. It simply doesn’t pay enough company tax to the ATO.

In 2000, an enhancement to the scheme was made by Peter Costello to refund excess imputation credits in cash. The purpose was simple – to make sure that every shareholder (taxpayer) gets the same benefit. This is what Shorten now proposes to axe.

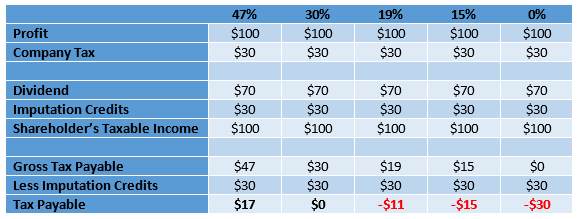

Let’s take an example to demonstrate the point. Suppose that a company makes a profit of $100, pays tax of $30, and then distributes a dividend of $70 to its shareholders. Because it has paid the full amount of company tax, it can fully frank the dividend. Consider five shareholders – with respective marginal tax rates of 47% (the highest), 30% (potentially another company), 19%, 15% (a super fund in accumulation phase) and 0% (a super fund in pension phase or an individual earning less than $18,200).

Dividend Imputation by Shareholder Tax Rate

For a shareholder paying tax at rate of 47%, both the dividend of $70 and the imputation credits of $30 are included in their taxable income. Tax of $47 is assessed, and then the imputation credits act like a tax rebate, meaning that the net tax payable is $17. On the profit of $100, the company has paid $30 in tax, and the shareholder $17 (total $47).

In the case of a shareholder paying tax at 30%, such as another company, the gross tax payable on the taxable income of $100 is $30. After deducting the imputation credits, the net tax paid is $0.

For shareholders paying tax at 19% or 15%, the imputation credits more than offset the gross tax payable. The excess imputation credits are then refunded in cash, meaning that the shareholder has in addition to the dividend, received a cash payment from the ATO. Finally, for a shareholder with the best marginal tax rate of 0%, they pay no tax and get the imputation credits refunded in full.

This table highlights two important points. Firstly, the total amount of tax paid to the ATO on company profits depends on the tax rate of the shareholder. If the shareholder is a low rate or 0% rate taxpayer, the Government’s take is small. Conversely, if the shareholder is paying tax at the top rate, company profits are effectively taxed at 47%. Whether this is right or wrong is arguable, but it is totally consistent with a progressive taxation system.

Secondly, it is utter nonsense by Shorten and his cronies to say that denying the refundability of excess imputation credits is closing a “tax loophole”. There is no loophole, but rather a system where every taxpayer gets the same benefit – their tax is reduced by the same $30 (reflecting the tax the company has paid). What could be more equitable than this?

MORE BUYBACKS AND SPECIAL DIVIDENDS

Clearly, some of the strong dividend paying stocks will look less attractive to investors. Telstra, which pays a fully franked dividend of 22c per share, is probably the best example. For a shareholder with a tax rate of 0% (such as a SMSF in pension phase or retiree with limited income investing outside super), on a purchase price of $3.40 per share, this translates to a yield of 9.2%. Take away the refunding of the franking credits, the yield is crunched to 6.5%. Still interesting, but a lot less exciting. Impact – the share price will fall.

The banks and other high paying dividend stocks could also be impacted.

But there will also be offsetting actions that some companies will take. Because the change won’t come into effect until the start of the 2019 tax year, some Boards will “read the tea leaves” and accelerate the payment of special dividends. Companies with strong capital positions and healthy franking account balances will undertake off-market buybacks. These allow companies to buy their shares back at a discount to the then market price, and are particularly attractive to zero rate taxpayers who can get their excess imputation credits refunded in cash. Take way this aspect, as Shorten proposes, and off-market buybacks as we know them could well be a thing of the past.

One thing we can be certain of is that Shorten’s proposal will become a hot political issue. And in due course, will be seen for what it is – a naked tax grab.