Losing the ability to earn an income to fund living expenses could run down savings levels and cause financial difficulty. As an adviser, you play an integral role in helping your clients recognise the importance of income protection and help them to manage their cash flow and any potential risks. However, for many clients the decision to hold income protection insurance comes down to affordability.

But what should your clients consider when deciding on how to structure their income protection cover? When thinking about whether insurance should be held inside or outside of superannuation, it is important to note that some of the key features remain the same, such as:

- Premiums are generally tax deductible under both ownership structures

- The after-tax cost of the premiums is the same for the client under both structures, and

- Upon claim, monthly benefit payments are taxed at the client’s marginal tax rate under both structures as payments are considered ‘ordinary income’.

This article will address the key differences between the two ownership options and look at how split insurance policies may provide clients with the best of both worlds.

Superannuation-owned income protection

Most superannuation funds offer insurance for their members. There are many benefits of this ownership structure however clients must also be aware of the potential pitfalls. The points below are the potential advantages and disadvantages to consider when it comes to owning income protection through superannuation.

Advantages

- Premiums can be funded from employer contributions, member contributions or by using their existing superannuation fund balance, which may assist clients in managing their cashflow and affordability of premiums.

- Clients can benefit from income tax savings by claiming a tax deduction for personal contributions or by contributing via a salary sacrifice arrangement using pre-tax salary which may provide cost savings on premiums.

- Premiums may be cheaper, particularly for group insurance policies that may also provide individuals with automatic acceptance up to a set level of cover with no medicals required.

- The trustee of the superannuation fund will generally withhold PAYG tax on benefit payments before the monthly benefit is paid to the client.

Disadvantages

- In addition to meeting the insurance policy definition of incapacity, the client must also meet the temporary incapacity condition of release under superannuation law before the trustee can pay the income protection benefit to the client (i.e. client must cease employment due to illness or injury to meet eligibility requirements).

- Payments may be delayed as benefits must generally be paid by the insurer to the trustee first.

- Premiums can erode retirement savings if clients don’t make extra contributions to negate premium cost.

- Contributions made to fund premiums count towards the contribution caps.

- Restricted to indemnity policies where the benefit amount is usually limited to what income the client earned 12-24 months before becoming temporarily incapacitated.

- Ancillary benefits such as critical illness benefits cannot be provided as benefits through superannuation are limited to a non-commutable income stream in substitution for the income the client was receiving before incapacity.

- Additional fees may be payable when funding premiums by way of rollover from another complying superannuation fund.

- Income protection benefits may cease if the life insured becomes permanently disabled and the trustee determines that the client no longer meets the definition of temporary incapacity.

Income protection outside of superannuation

Owning income protection outside of superannuation can provide clients with more product features and flexibility when compared with owning insurance inside superannuation. Below are some of the main advantages and disadvantages when it comes to having a personally owned income protection policy.

Advantages

- Premiums are generally tax deductible for the client if they are both the life insured and the policy owner.

- Can provide protection even if the life insured is not employed at the time of incapacity.

- Ability to choose between indemnity value or agreed value cover – under agreed value cover a claim payment is generally based on the client’s income at the time of application (even if their income has since reduced).

- Policies are customisable and available under different ownership structures (e.g. may be used for business purposes, such as covering business expenses in the event of illness or injury).

- Policies can provide more comprehensive coverage, including ancillary benefits such trauma, rehabilitation expenses, relocation benefits and carer costs.

- May be able to exchange ongoing payments for a lump sum benefit.

Disadvantages

- If the income protection policy provides for benefits of an income and capital nature, the ATO’s view is that only that part of the premium attributable to the income benefit is deductible [1].

- Pre-existing medical conditions and lifestyle factors such as smoking may impact the cost of premiums (whereas group insurance inside superannuation may have automatic acceptance).

- As premiums are generally paid personally from after-tax income [2], a waiting period that meets a client’s needs may not be affordable, particularly if no sick pay is available

- As PAYG tax is generally not withheld from benefit payments, clients must remember to declare the whole amount received on their annual tax return.

Tip

When it comes to helping clients compare life and TPD insurance cover, it’s important to look at both the value of the cover and how much it will cost.

AIA has a helpful tool called “Comparison of insurance premiums funded inside vs outside of super” which compares the value of $1,000 worth of premium and how much it will cost a client when paying with:

- Pre-tax dollars (i.e. by way of salary sacrifice or personal deductible contributions) inside superannuation, versus

- Paying for premiums personally with after-tax dollars.

This tool can be used as a visual guide to help clients compare the gross cost of premiums at each individual marginal tax rate.

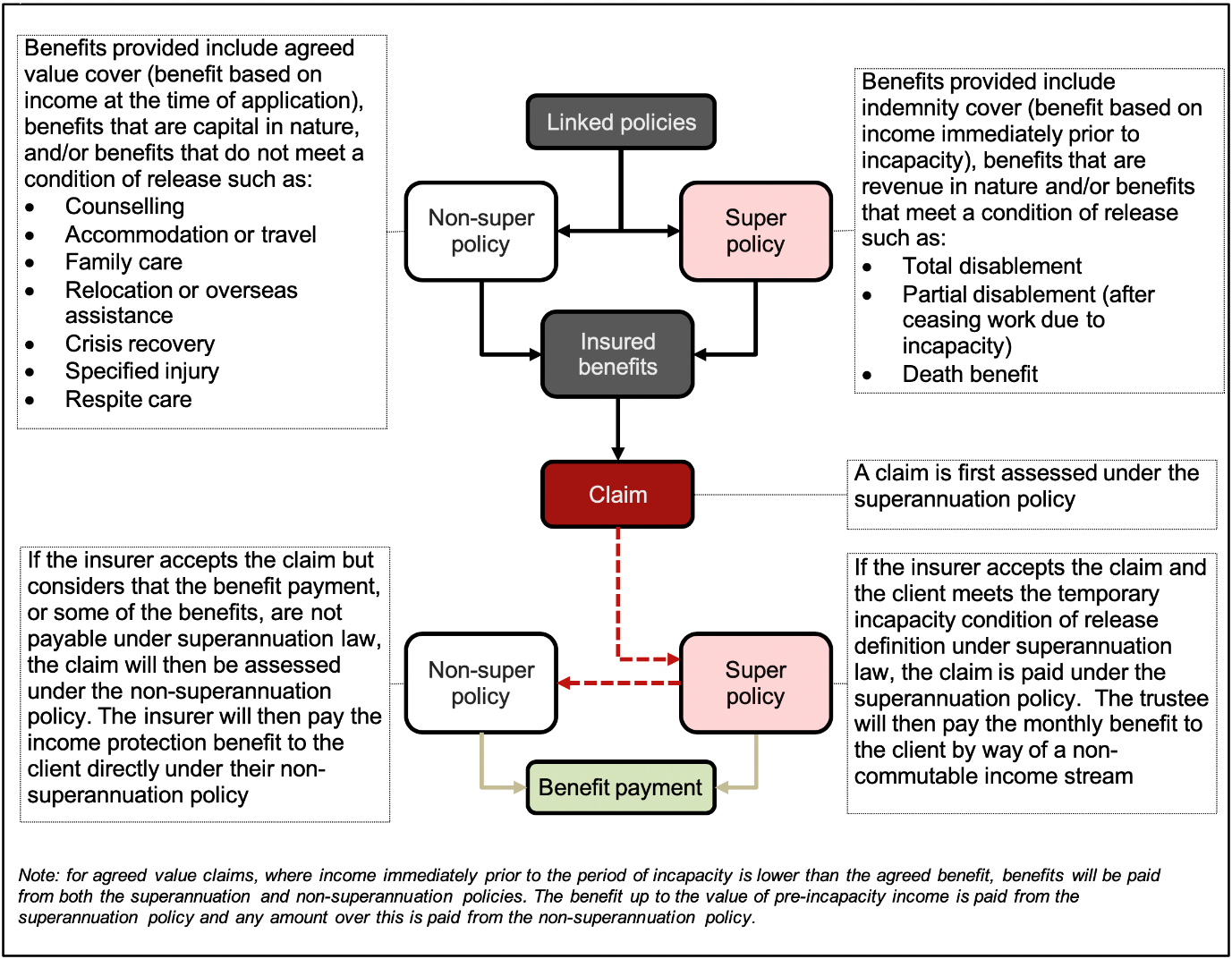

Split policies

Split polices are an alternative option for clients who want the best of both ownership structures. Having a split policy can provide clients with the benefits of owning insurance through superannuation whilst also providing them with enhanced cover and ancillary benefits outside of superannuation. Two policies are issued where one is owned within superannuation by the trustee of the superannuation fund on behalf of the client and the second policy is personally owned by the client who is the life insured. Both polices must remain active and if one policy lapses or is cancelled, the linked policy will also be cancelled.

The diagram below summarises how a linked insurance policy may be structured.

When it comes to weighing up the option of having a split policy, the same pros and cons of having insurance inside versus outside superannuation apply. For example, clients can tailor what cover is inside and outside of superannuation and not compromise their level of cover. This is because a linked policy outside of superannuation gives clients access to enhanced cover and optional benefits that are not available inside superannuation.

However, there are some extra factors that clients should consider when it comes to split policies, such as:

- The client cannot choose which policy they are paid under upon claim time. If an income protection claim is made, it will firstly be assessed under the superannuation policy.

- The insured monthly benefit amount under both income protection policies must be the same at all times.

- The total benefit payable under both policies cannot exceed the total insured monthly benefit under the superannuation income protection plan.

- If the insured monthly benefit is reduced under either the superannuation policy or the linked benefit under the ordinary policy, the same reduction may apply to the other policy.

Comparison of policies owned inside versus outside of superannuation

The table below provides a summary of the key differences between the three ownership structures.

Summary

Making the right choice when purchasing income protection insurance will depend on the different requirements of each client. For example, clients who have sufficient cash flow may be better suited to having income protection outside superannuation whereas clients with uncertain cash flows, such as small business owners or young families with tight finances, might be better off insuring their incomes inside superannuation – noting that clients’ situations and needs may change over time.

As this is a complex area for clients to navigate alone, it is important for advisers to explain to their clients the advantages and disadvantages of insurance policy ownership and the benefit of regularly reviewing their insurance needs.

[2] It is possible for an employer to allow their employees to salary package (i.e. salary sacrifice) their income protection premiums. Where this is the case, the employee may also benefit from income tax savings by forgoing their future entitlement to pre-tax salary or wages in exchange for the employer funding the cost of income protection premiums.

[3] The ATO has provided guidance stating that the portion of the premium attributed to benefits that are capital in nature are not deductible https://www.ato.gov.au/Individuals/Income-and-deductions/Deductions-you-can-claim/Other-deductions/Income-protection-insurance/

Source: AIA TECE Team