On 21 July 2020, the Government announced a range of proposals to the JobKeeper and JobSeeker payments as existing arrangements are set to expire in late September 2020. After 27 September 2020, the JobKeeper payment is proposed to reduce to $1,200 per fortnight (pf) for full-time workers and $750 pf for part-time workers, with a further reduction from 4 January 2021.

The Coronavirus Supplement of $550 pf for the JobSeeker payment will reduce to $250 pf from 25 September until 31 December 2020. There are further proposals for the income test taper rate and access to the JobSeeker Payment. As we are yet to see legislation, these proposals are subject to change.

Certain tax concessions to assist businesses were extended and have been legislated.

The Government announced further changes to early access to super owing to COVID-19. Eligible individuals can access up to $10,000 of their super in 2020/21. The deadline for application will be extended from 24 September 2020 to 31 December 2020. At this stage, no additional amounts can be accessed beyond this date under this condition of release. We will keep you informed about any developments.

JobKeeper Payment extended

The JobKeeper Payment will be extended to 28 March 2021 for eligible businesses and not-for-profits. However, from 28 September 2020 the JobKeeper Payment rate will reduce. Prior to this announcement, the JobKeeper Payment was to cease on 27 September 2020.

Businesses and not-for-profits eligible for extended JobKeeper Payment from 28 September 2020

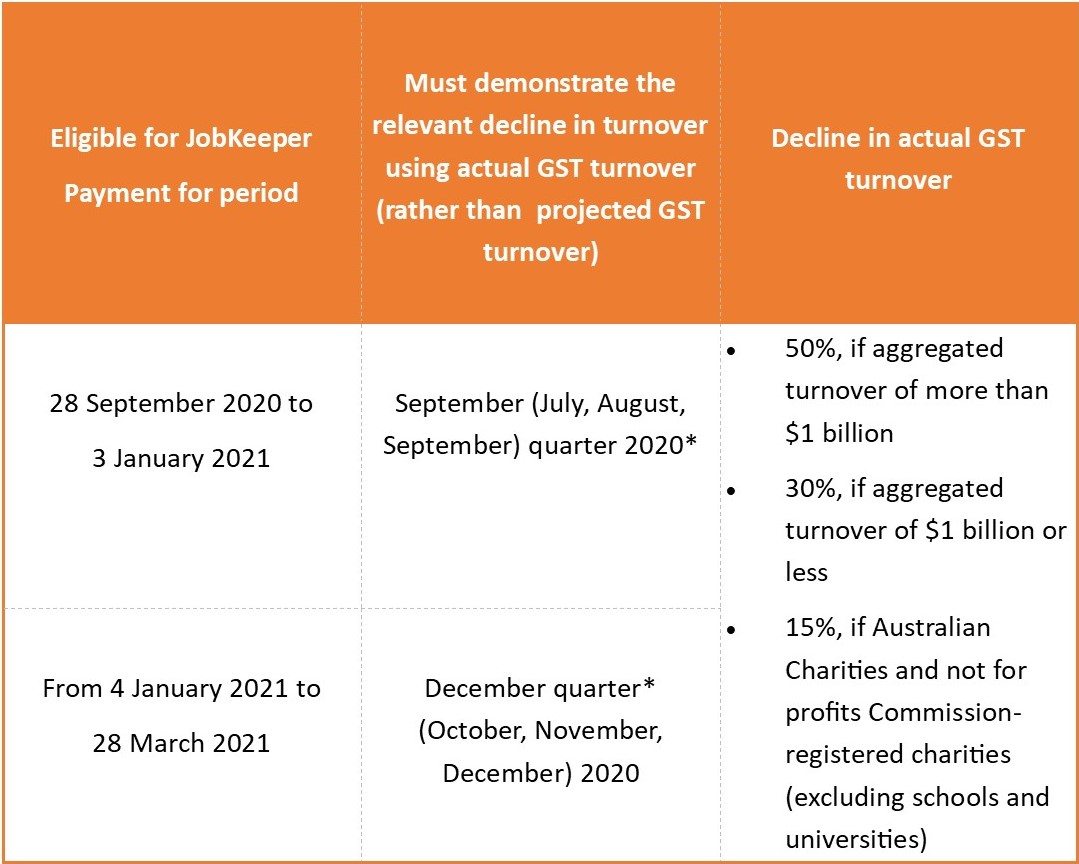

From 28 September 2020, businesses and not-for-profits will need to reassess their eligibility for the JobKeeper Payment by demonstrating they have suffered an ongoing significant decline in turnover using actual GST turnover (rather than projected GST turnover) relative to a comparable quarter last year (2019), as shown in the table below.

In the 7 August 2020 update, it was announced that businesses will only need to show that their GST turnover had fallen over one quarter, instead of multiple quarters, in order to be eligible for the scheme’s extension.

Other eligibility rules for businesses and not-for-profits and their employees remain unchanged.

* relative to comparable period, generally the corresponding quarters in 2019

As the deadline to lodge a BAS for the September quarter or month is in late October, and the December quarter (or month) BAS deadline is in late January for monthly lodgers or late February for quarterly lodgers, businesses and not-for-profits will need to assess their eligibility for JobKeeper in advance of the BAS deadline in order to meet the wage condition. That is, the requirement to pay eligible employees in advance of receiving JobKeeper Payment in arrears from the ATO. The Tax Commissioner will have discretion to extend the time the entity has to pay employees in order to meet the wage condition, so that entities have time to first confirm their eligibility for the JobKeeper Payment.

Revised JobKeeper eligibility criteria for employees

On 7 August 2020, it was also announced that to be eligible for the JobKeeper Payment from 3 August 2020, the employee must have been employed by the business or not for profit as at 1 July 2020. Previously this date was 1 March 2020. This should allow more people to be eligible for the scheme.

To be eligible in the extension period an employee:

- has to be currently employed by an eligible employer (including a stood down or re-hired employee)

- is for the eligible employer either:

- a full-time, part-time or fixed-term employee at 1 July 2020; or

- a long-term casual employee (employed on a regular and systematic basis for at least 12 months) as at 1 July 2020 and not a permanent employee of any other employer.

- was aged 18 years or older at 1 July 2020 (if the employee was age 16 or 17 the employee may be eligible if they are independent or not undertaking full time study).

- were either:

- an Australian resident (within the meaning of the Social Security Act 1991); or

- an Australian resident for the purpose of the Income Tax Assessment Act 1936 and the holder of a Subclass 444 (Special Category) visa as at 1 March 2020.

- was not in receipt of government parental leave or Dad and Partner Pay during the JobKeeper fortnight; or worker’s compensation payments for their total incapacity for work.

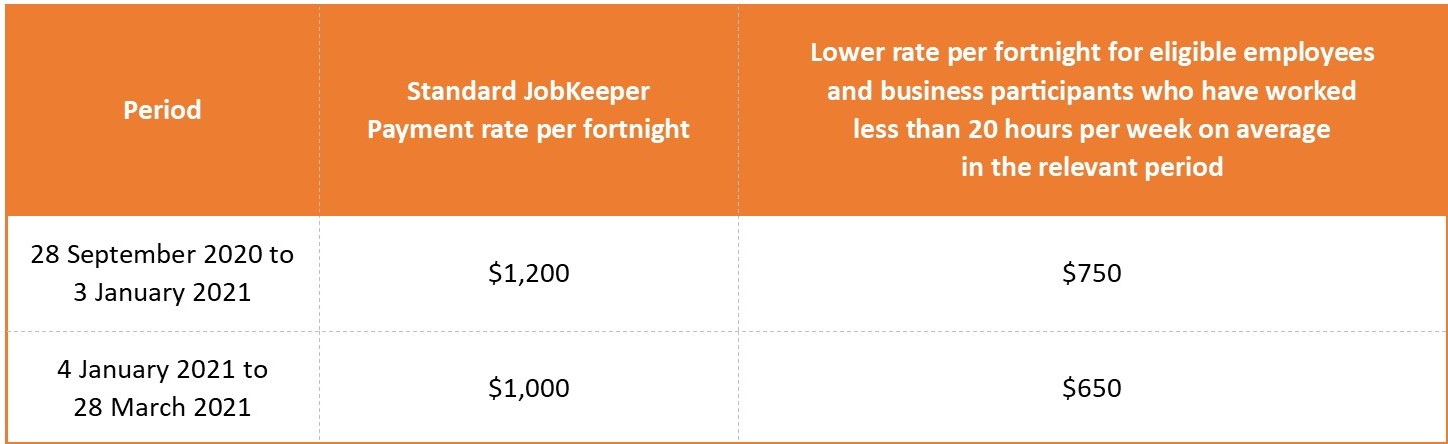

JobKeeper Payment rate

From 28 September 2020, the standard rate of JobKeeper Payment will reduce in two stages and lower payment rates apply to employees (and eligible business participants) of eligible businesses and not-for-profits who have worked less than 20 hours per week on average, in the four weekly pay periods before 1 March 2020 or 1 July 2020 from 3 August 2020. Please see the table below.

The Commissioner of Taxation will have discretion to set out alternative tests where an employee or business participant’s hours were not usual during the February and/or June 2020 reference period (the period with the higher number of hours worked is to be used for employees with 1 March 2020 eligibility). For example, this will include where the employee was on leave, volunteering during the bushfires, or not employed for all, or part of, February or June 2020.

Businesses will need to nominate which payment rate applies for each eligible employee or eligible business participant.

JobSeeker Payment: Coronavirus Supplement, income test and waiting period changes

Extended and reduced Coronavirus Supplement

Payment of the Coronavirus Supplement has been extended to 31 December 2020. From 25 September 2020 to 31 December 2020, the Supplement amount will be reduced to $250 pf. This supplement is paid in addition to the actual JobSeeker Payment.

Existing JobSeeker Payment recipients and new JobSeeker Payment recipients will be eligible for the Coronavirus Supplement up until 31 December 2020. The Government has not indicated whether it can extend this supplement beyond this date.

Eligibility criteria for the Coronavirus Supplement remains the same.

Changes to the JobKeeper Payment may make recipients of that payment eligible for the JobSeeker Payment.

Adjustments to the JobSeeker Payment income test – 25 September to 31 December

Personal Income test

The income free area for JobSeeker Payment recipients will increase from $106 pf to $300 pf. This means recipients may receive income up to $300 pf without any reduction in JobSeeker Payment.

Under the income test, every dollar received over $300 per fortnight will reduce JobSeeker Payment by 60 cents. Currently the JobSeeker Payment is reduced by 50 cents for every dollar received between $106 and $250 per fortnight and by 60 cents thereafter.

This income test is applied to the JobSeeker Payment only. If a client is eligible for any JobSeeker Payment they will get the full Coronavirus Supplement.

Partner Income Test

The reduction rate under the Partner Income Test will increase from 25 cents to 27 cents. Partners of JobSeeker Payment recipients may receive up to $3,086.11 pf or $80,238.89 per annum before the JobSeeker Payment cuts out. Note, this assumes the JobSeeker Payment recipient has personal income below the income free area.

Asset Test and Liquid Asset Waiting Period to apply from 25 September 2020

The Asset Test will apply from 25 September 2020. For example, single homeowners with assessable assets of $268,000 or more will not be eligible for JobSeeker Payment. Partnered homeowners may have up to $401,500 in combined assessable assets.

The Liquid Asset Waiting Period (LAWP) of up to 13 weeks will be reinstated and the Income Maintenance Period (IMP) will continue.

The Ordinary Waiting Period, Newly Arrived Resident’s Waiting Period (NARWP) and the Seasonal Work Preclusion Period will continue to be waived until 31 December 2020.

Mutual Obligation Requirements

As previously announced Jobseekers’ mutual obligation requirements were gradually reintroduced from 9 June 2020.

Instant asset write-off thresholds for small businesses extended until 31 December 2020

Small businesses with aggregated annual turnover of less than $500 million may be eligible for an increased instant asset write-off on assets of up to the value of $150,000 from 12 March 2020 until 31 December 2020. The measure was set to finish on 30 June 2020, but the Government passed legislation to extend the measure until 31 December 2020.

The measure applies to new or second-hand assets first used, or installed ready for use, between 12 March 2020 until 31 December 2020 (inclusive). Certain assets are excluded, for example, horticultural plants and capital works deductions. There are limits to deductions for certain cars. The threshold applies on a per asset basis, so eligible businesses can immediately write-off multiple assets. Clients should confirm the entitlement to the tax deduction with their accountant.

Backing business investment

The Government has introduced a time limited 15 month acceleration of depreciation deductions for businesses with aggregated turnover below $500 million. Legislation to support this measure has already passed.

The deduction of 50% of the cost of an eligible assets on installation will be allowed, with existing depreciation rules applying to the balance of the asset’s cost. Eligible assets are new assets that can be depreciated under Division 40 of the Income Tax Assessment Act 1997 (ie, plant, equipment and specified intangible assets, such as patents) acquired from 12 March 2020 and first used or installed by 30 June 2021. Second-hand assets, or buildings and other capital works are not eligible assets. This concession will support business investment and economic growth over the short-term. Clients should confirm the entitlement to the tax deduction with their accountant.

More information

If you would like more information please contact your Financial Adviser or Accountant.

Source: Australian Executor Trustees Ltd – 11 August 2020