If you’re aged 65 or over, you may be eligible to make additional super contributions of up to $300,000 (or $600,000 per couple) from the proceeds of selling your home.

These are known as ‘downsizer contributions’ and they can be made on top of the existing contribution caps, without having to meet certain contribution rules and restrictions.

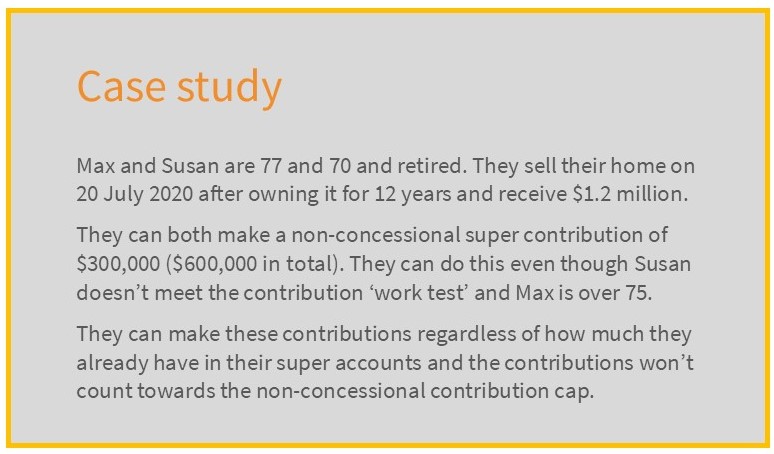

How does the strategy work?

The downsizer contribution rules have removed some of the existing barriers that prevent or restrict your ability to make super contributions later in life.

Provided certain other conditions are met (see below) it may be possible to contribute up to $300,000 per person (or $600,000 per couple) from the proceeds of selling your home.

The contributions won’t count towards your concessional (pre-tax) or non-concessional (after-tax) contribution caps and there is no maximum age limit. Also, the ‘work test’ (for people aged 67 to 74) and the ‘total super balance’ test won’t apply.

Key conditions

There are a number of conditions you’ll need to meet to be eligible to make downsizer contributions, including:

- You must be aged 65 or over at the time you make the contribution.

- The property must have been owned by you or your spouse (but not necessarily both) for at least 10 years prior to the disposal.

- The property must qualify for the main residence capital gains tax exemption in whole or part, so properties held purely for investment purposes won’t qualify.

- You must make the contribution within 90 days of the change of ownership.

- You need to make an election to treat the contribution as a downsizer contribution.

- You cannot claim the contribution as a tax deduction.

- Other conditions may also apply.

Other key considerations

There are some key issues that should be considered when assessing whether making downsizer contributions could be a suitable strategy, including:

- The property being sold to fund the contributions doesn’t have to be your current home. It can be a former home which meets the requirements. Also, you don’t need to purchase another home.

- Once contributed, downsizer contributions will count towards your ‘total super balance’ which could impact your capacity to make future contributions.

- Downsizer contributions can’t be transferred into a tax-free ‘retirement phase income stream’ if you have used up your ‘transfer balance cap’. The transfer balance cap is $1.6 million in 2020/21.

- If you have used up your transfer balance cap, the contribution must remain in the ‘accumulation phase’ of super, where investment earnings are taxed at a maximum rate of 15%.

- Money held in the accumulation or retirement phase of super is assessed for both social security and aged care purposes.

For more information, please visit the ATO website at www.ato.gov.au

Seek advice

Please speak to your Pinnacle adviser who can help you assess whether downsizer contributions suit your needs and circumstances.

Source material: MLC