Like many Australians, you may have dipped into your super early as part of the government’s Coronavirus financial hardship scheme. While the extra funds can come in handy right now, it’s important to keep sight of the bigger picture.

If you lost your job or had your hours reduced due to the impact of the Coronavirus, you may have taken advantage of the government’s early release of super scheme and dipped into your super to help with your living expenses.

Once you’re in a more comfortable financial position, it may be time to think about how you will rebuild your super balance to minimise the long-term impact on your retirement savings. This is especially important when you’re young because of the power of compounding returns over time. You can use the government’s moneysmart super withdrawal estimator to see how much of an impact the withdrawal may have on your retirement, so you can work out how much you need to rebuild.

Here are four simple suggestions for how to get your super back on track again.

1. PUT ANY SPARE MONEY BACK IN YOUR SUPER

Keep in mind, however, that the ATO is imposing penalties for anyone they determine has taken money out of super and then recontributed it for the sole purpose of obtaining a tax deduction. You can read more about it on the ATO website.

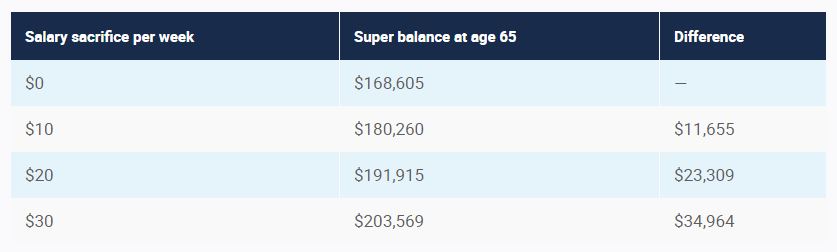

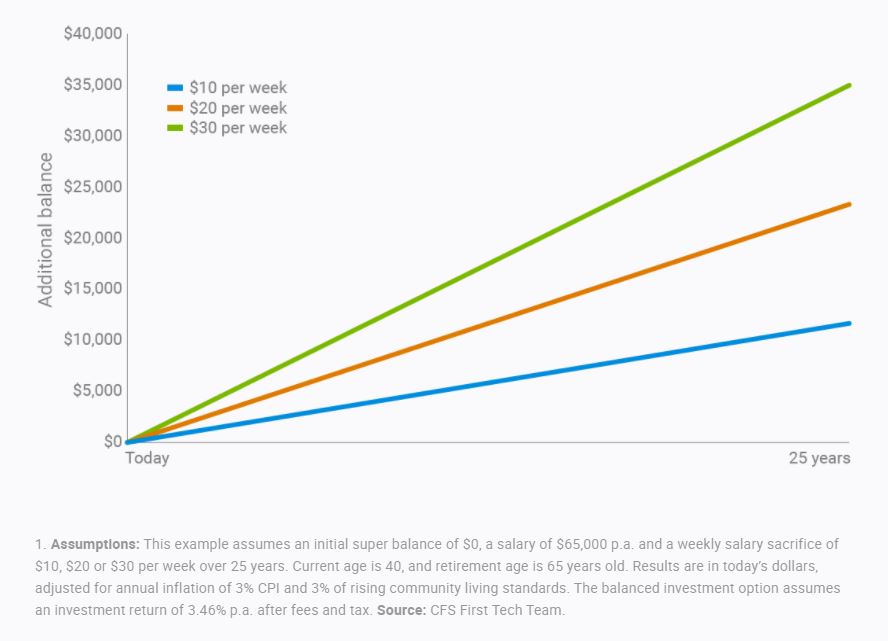

2. ADD A LITTLE BIT EXTRA TO YOUR SUPER EACH PAY DAY

Regularly putting in extra money to top up your super can make a big difference to your balance over time. For example, this chart shows the difference contributing a small amount each pay could potentially make to your super balance at retirement.1

3. PUT A LUMP SUM TO GOOD USE

- a redundancy payout

- a tax refund

- an inheritance

- the proceeds from a sale, such as a car or your house.

Just remember that there are limits around how much you can contribute to super each year. Currently, you can make up to $25,000 in before-tax (concessional) contributions and $100,000 in after-tax (non-concessional) contributions each financial year.2 If you go over these caps, you may have to pay additional tax.