So far, it’s proven difficult to eliminate the Coronavirus – even though some countries have been willing to impose an almost-complete lockdown. With much of the world about six months in to a Coronavirus-induced lockdown, what we know so far is that the virus subsides and surges depending on the severity of social-distancing measures. What this suggests is a vaccine may be the only hope in extinguishing the Coronavirus completely. But how far away are we from an effective vaccine?

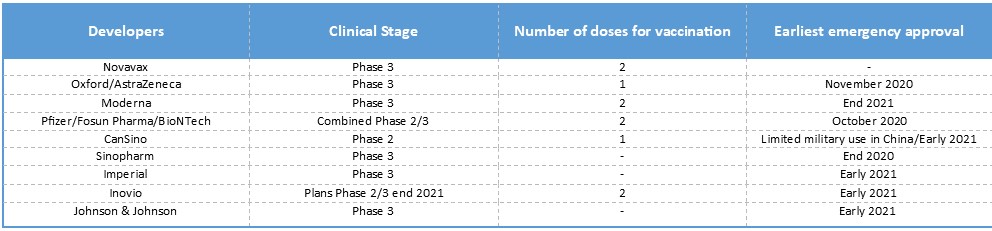

Let’s start with the good news: massive resources have been deployed worldwide to develop a vaccine and scientists have so far made impressive progress. As of mid-October, the World Health Organisation has listed more than 170 vaccines in various stages of development. Scientists have gone from discovering the virus to supplying more than 170 candidates in record time, with 65 vaccines in human trials (as at 13 October) across three phases: Phase 1 for safety, Phase 2 for efficacy and dosing, and Phase 3 for efficacy in a large group of tens of thousands of people. While five candidates have completed Phase 3 (at the time of writing), it may take some months before more conclusive evidence is published about their efficacy. Some promising vaccines are in listed the table below:

Sources: MKP, The Guardian, Citi, Who and Companies’ Websites.

How might financial markets react to a vaccine?

It’s likely that the approval of a vaccine will lead to a rally in share markets, at least in the short term. The scale of the initial reaction will depend on two factors: firstly, the information disclosed on announcement surrounding the efficacy and availability of the approved vaccine, and secondly, the extent to which the positive news has already been “priced in”. It is difficult to estimate the extent to which financial markets have priced in good news on a vaccine. Research by UBS has suggests that share markets priced in around 33%–40% implied probability of a vaccine being approved.

During this initial rally, cyclical sectors and stocks that have been worst affected will likely outperform the rest of the market. Those sectors include airlines, hotels, retailers, energy and banks. So far, the US share market has outperformed many others – including Australia. Markets in developed countries that are likely to have early access to a vaccine could play catch-up with the US. The impact on emerging markets may be more nuanced, given the uncertain timing on the availability of vaccine in less developed nations.

It is also possible that the approval of a vaccine will signal the start of a significant rotation from growth stocks (mainly large-cap technology and internet stocks) to cyclical and value stocks (such as materials, consumer discretionary and banking stocks). But while cyclical stocks may initially outperform, it’s debateable whether or not this will signal the beginning of a long-term rotation. A significant rotation requires investors being convinced that most of the rise in revenue of technology stocks is driven by a temporary boost to demand caused by Coronavirus, not a structural shift, and the conclusion that growth stocks are overvalued. The relative valuation of growth versus value stocks matters. The September sell-off in growth stocks has suggested investors may already be concerned by their high valuations. The trailing 12-month price-to-earnings ratio of the NASDAQ Index, which can be seen as a broad proxy for growth stocks, was 32.2 compared to the September peak of 34.3 and the long-term median of 19.14.

The approval of a vaccine will mark the beginning of a normalisation process of unknown duration for world economies and financial markets. This normalisation process may take some time, with financial markets pulled in two opposite directions. On the positive side, corporate revenue and earnings will rise as economic activity and employment recover. On the negative side, central banks and governments will face increasing pressure to reduce support stimuli as economies recover at some point in the future. As in most investment issues, sequencing matters.

It is impossible to predict the precise pace and path of development during this normalisation period. Much will depend on economic data, Coronavirus developments and the policy reactions of central banks and governments. Major central banks are aware of the risks of withdrawing liquidity too rapidly. For example, the US Federal Reserve’s decision to revise its long-term monetary policy framework from targeting inflation of 2% to targeting average inflation of 2% is acknowledgement that it needs to maintain supportive policy for some time after inflation reaches its target. Given central banks are determined to maintain low interest rates and are willing to let inflation overshoot their targets, the positive impacts from improving earnings expectations could dominate after the initial approval of a vaccine. But over time, markets may become more concerned about the sustainability of low interest rates. The point of maximum risk could come when the global economy has recovered to such an extent that financial markets start to price in the main central banks’ tightening policies. It is difficult to identify this tipping point but it is unlikely to occur until at least 2022.

While a vaccine would certainly be welcome, the recent news that AstraZeneca has placed the Phase 3 trial of its vaccine on hold is a reminder that there is still a possibility that no vaccine is approved – either in 2020 or even in 2021. This is probably the worst-case scenario for financial markets. Investors may be forced to reprice their expectations that earnings will recover rapidly next year. However, this negative impact will be offset to some extent by more fiscal and monetary stimuli.

What do we need to consider about a vaccine?

There is a reasonable possibility, but not a certainty, that at least one vaccine will be approved for emergency use by regulators by the end of 2020. While this is good news, it will probably not be sufficient to send the world economy back to normal. Even after a vaccine is approved, there are still a number of challenges which may take months, if not years, to overcome.

The first challenge is the scale and speed of production for an approved vaccine. Virologists have estimated that 50% to 60% of the population needs to be vaccinated and/or infected with Coronavirus to achieve herd immunity. But with a world population of around 7.8 billion, this means roughly 3.9 billion doses are needed. Several pharmaceutical companies, like AstraZeneca and Pfizer, are already taking steps to quickly ramp up production if a vaccine is approved. The most optimistic estimate is, if all promising vaccines are approved, that 10 billion doses can be produced in 2021. However, while this figure is encouraging, it is also a very optimistic scenario since some candidate vaccines will likely fail.

It is also unclear who will have access to an approved vaccine. If approved, it seems most of the initial production of vaccines will be taken up by more developed nations, while less-developed countries may need to wait their turn. For example, while the United States has pre-ordered 800 million doses across major developers, Australia currently has 25 million doses on pre-order with one. Current geopolitical tensions have added another element of uncertainty. Two of the most promising vaccine candidates are being developed by Chinese companies Sinopham and CanSino, which has already been given limited approval for military use despite still being in trials. If either is successful, would China share those vaccines with the rest of the world?

Another challenge is the efficacy of any approved vaccines. Vaccines work by activating the immune system without disease and can be made in various ways – for example, with weakened or inactivated viruses, proteins from a virus, or a viral protein grafted onto an innocuous virus. The challenge is that vaccine-induced immunity tends to be weaker than immunity that arises after an infection. Many medical experts have likened a Coronavirus vaccine to the seasonal flu shot – it helps to limit the spread of the flu but does not eliminate it altogether. In addition, governments are under pressure to authorise the emergency use of a vaccine, and some authorities have indicated they will approve a vaccine for emergency use even if it only has 50% efficacy.

Finally, several leading candidates are relying on technology that’s never been used before in approved vaccines. Moderna’s vaccine is a piece of RNA that encodes a coronavirus protein, while Oxford and AstraZeneca’s vaccine attaches a coronavirus protein to a chimpanzee adenovirus.

Source: George Lin, Senior Investment Manager, Colonial First State