Tailored advice plays a vital role in all stages of the retirement journey. And clients increasingly expect advisers to focus on more than just their financials to improve long-term outcomes and resilience – making a solid case for holistic advice.

When a person enters retirement and moves out of the traditional wealth accumulation phase, they experience change on many levels. This is not just from a financial perspective, but also emotional and psychological – particularly as they get used to a life without the structure of work, a regular income or the same social networks.

These changes can amplify the issues, challenges and risks for people in retirement, making the need for support all the more important.

Retirement-specific frameworks play a role in helping to solve the problem of uncertainty during this time. They guide retirees to consider the risks and challenges, products, portfolios and strategies out there to assist them. This can go a long way to providing better risk management and stability.

It’s clear that there’s never been a more pressing time for advisers to address advice holistically. Here we look at the various phases of the retirement journey to see how holistic advice fits in – and how your adviser can help you to become more resilient, adapt to change and improve financial, emotional and psychological outcomes.

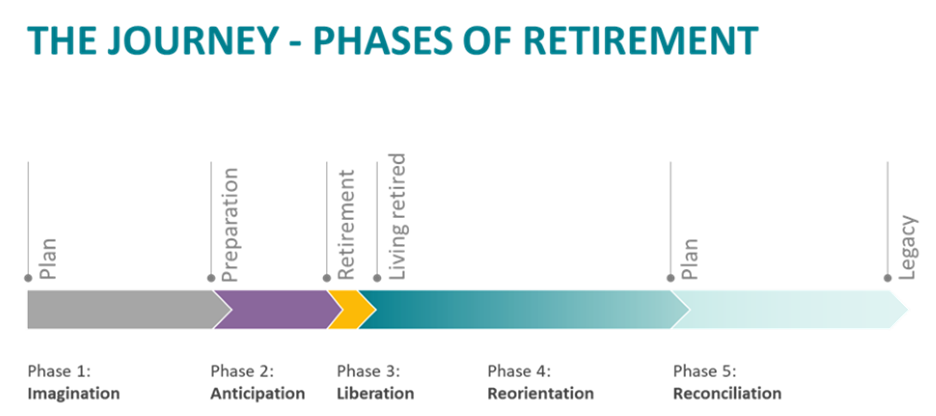

Imagination and anticipation

Planning, preparedness and education have a significant impact on the confidence and certainty you may have in retirement. The imagination phase gives you time to imagine what retirement could look like and the anticipation phase helps you to set expectations and get mentally ready to retire.

It’s an opportune time to start defining timeframes and goals. In these phases, you should consider your financial objectives, but also the non-financial aspects of retirement preparedness. This includes looking at your emotional, psychological and practical needs.

A study by Professor Gail Matthews at the Dominican University of California1 reveals that those who didn’t just think about goals, but wrote them down with action commitments before sharing with a friend and doing weekly progress updates, had a 95 percent rate of achieving them. Meanwhile, those who thought about their goals but took no action only had a 53 percent rate of achievement.

At this point, your adviser may ask you to consider a series of questions, including, when will your kids likely leave school or home, when they’ll repay all debts, if you are planning on relocating or downsizing, and what hobbies you may like to spend time on in retirement years. Having these type of conversations about values is also important so you can make aligned decisions. It’s also critical for your adviser to set expectations around how much money you might have in retirement and the kind of lifestyle you can realistically afford.

If there’s one thing to remember during the planning stages, it’s that every person’s needs are unique. This is why holistic advice can help to uncover the nuances so your adviser can support you in achieving individual goals, while navigating any obstacles that might come your way.

Liberation (the honeymoon period)

The early years of retirement, or liberation phase, are the ultimate test of goals and expectations – where financial risks can be amplified for many new retirees.

According to Allianz Retire+ research2, 21 percent of retirees say the fear of loss-causing market swings keeps them awake at night. Further, only 33 percent of current and prospective retirees feel secure in the event of an economic downturn.

COVID-19 and stock market volatility haven’t helped this sentiment either, casting a dark shadow on confidence. So while you might feel liberated to finally be in retirement, you may also feel disenchanted, especially if you didn’t have the choice to retire, or had to make a hasty decision. Due to the current economic uncertainty, 75 percent of Australians are now taking a more conservative approach to retirement3. Spending less and feeling more risk averse.

In fact, polling from Allianz Retire+ suggests that 38 percent of clients have deferred retirement in the past 12 months. The reasons for this vary: while some are waiting to recoup COVID-19 market impacts on portfolios, others delayed because planned travel was restricted or stayed working simply to have an activity to fill the day4.

Building a network for career advice, counselling services and a library of resources can play a critical role throughout this phase. Advisers offering education and support can help you make good decisions, so you can feel more confident about the future.

Reorientation, reconciliation and legacy

The next three phases of the retirement journey are reorientation, reconciliation and legacy. It’s during these periods that there are new risks, challenges and big decisions to consider.

Recent PIMCO research5 revealed five key risks that clients prioritise when making their retirement income plans. The first is health risks (65%) such as unforeseen medical expenses, followed by market risks (58%) like volatility, inflation and insufficient returns. Longevity risk or life expectancy was a seen as a key risk for almost half (46%). The final two were political risk (42%), including policy changes and tax rates, and personal or household risk (39%) which included non-health-related expenses.

Sheena Stow-Smith, Managing Director of AdviceLink, said the longevity piece is an important consideration. While the average life expectancy for a 65-year-old male is 85 years and for females 876, she said advisers shouldn’t rely on this average and should consider taking a more nuanced and holistic approach, factoring in the individual’s current situation and potential obstacles or future risks.

Some life-changing decisions during these three phases of retirement might include downsizing or transitioning into aged care, the latter of which can be “stressful, emotionally charged and unsettling,” Stow-Smith said.

This is where building an advice network with specialists in the earlier phases can be beneficial to plan and prepare.

You as the client might also begin to consider the legacy you want to leave behind. You may look into intergenerational wealth transfer and look at your current investment portfolios and consider more aggressive and growth oriented profiles.

A retiree’s age is significantly correlated with bequest motives for future generations and philanthropy. The desire to leave wealth to the next generation increases slightly with age, while the desire to leave wealth to charitable goals decreases slightly7.

The value of holistic advice

Your adviser can play a crucial role at the critical junctures in a retiree’s life, improving your resilience and wellbeing by considering broader circumstances and how you link to financial outcomes.

The financial services industry is already well-versed in getting to know a client’s money, assets, liabilities, products and goals through goals-based advice. Your Adviser at Pinnacle Wealth Management will take the next step, being a more holistic view of your needs and circumstances, including health, market and longevity risks, which we help to address your long-term interests.

Source: Allianz Retire+

- Professor Gail Matthews, Dominican University of California, Goals Research Summary, February 2020.

- Allianz Retire+, survey of 702 current and prospective retirees across Australia, published by NEXT CHAPTER Research, 2019.

- NEXT CHAPTER Research – Based on an Allianz Retire+ survey in 2019 of 702 current and prospective retirees across Australia.

- Crucial Conversations Webinar, Life-Changing Decisions – Best Made With Good Advice, Part 3, 2021.

- PIMCO, Managing Misbehaviour: Rational Choice in an Uncertain Retirement – Behavioral Insights, August 2021.

- AIHW, Older Australia at a glance, September 2018.